PwC: Insurance CEOs Optimistic About Growth

While insurance continues to be one of the most disrupted sectors in the global economy and insurance CEOs are more concerned about the pace of technological change than CEOs in any other industry, more than 90% of insurance CEOs are confident about their own organisation’s revenue prospects over the next three years.

This year 100 insurance CEOs participated in PwC’s 21st Global CEO Survey. The findings show insurance CEOs share a generally positive outlook, but actual growth has typically failed to live up to expectations.

Key findings

- Nearly half [49%] of insurance CEOs are planning a new strategic alliance or joint venture to drive profitability and growth over the next 12 months

- Half of insurance CEOs believe that global economic growth will improve over the next 12 months, up from only 19% in 2017

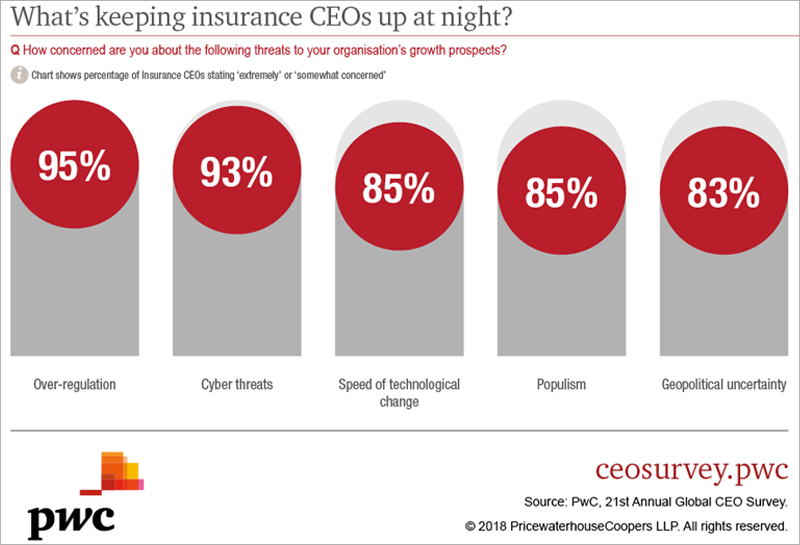

- Insurance CEOs 3 biggest concerns are over-regulation [95%], cyber threats [93%] and speed of technological change [85%]

- More than 80% of insurance CEOs are concerned about shortages of digital skills within the industry and within their workforce, which is the highest percentage of any industry

Arthur Wightman, PwC Bermuda leader and Insurance leader, says, “Among the many reasons for the high confidence of CEOs in the insurance industry is that the anticipated disruption from incoming competitors, like InsurTech and digital platform players, hasn’t materialised like the industry initially feared. Partnership, not rivalry, with new entrants is the order of the day.

“Substantial opportunities are on the horizon as a new generation of predictive analytics and AI transforms insurers’ ability to detect, anticipate and avert risk.”

Notable possibilities include RegTech, which can not only strip out costs in labour-intensive areas such as ‘know your customer’ requirements, but also strengthen risk management and improve the reliability of compliance.

Mr Wightman says, “Prospects for the Bermuda market remain good in spite of consolidation. Bermuda has a sustainable future based on the concentration of talent and its ability to find innovative insurance solutions, such as closing the global protection gap.”

Matthew Britten, PwC Bermuda Insurance partner, says, “The grounds for optimism among insurers include the increasing digitisation of the global economy and resulting shift in customer preferences.

“This opens up a range of new opportunities to both dramatically modernize processes to enhance customer interactions while reducing costs, and to meet the accelerating need to provide innovative insurance coverage against the nature of the intangible risks that are emerging as a result, such as we have already been seeing with cyber insurance.”

He noted that 40% of CEOs from across all industries are now extremely concerned about cyber threats, compared to 24% in 2017.

“So it is probably not surprising that we are seeing more re/insurance carriers offering stand-alone cyber insurance protection, and also a broadening of coverage, providing both first party and third party liability protection and coupling this with loss mitigation and incident response services.”

Successful insurers take both their technological capabilities and their readiness to innovate into the mainstream of their business.

“The successful re/insurers are going to be those that are prepared to capitalize on these new opportunities, while those weighed down by legacy and other long-term issues are going to be challenged,” he says.

Clear strategy and roadmap to get up to speed

More insurance CEOs are concerned about the pace of technological change [85%] than leaders in almost any other industry. Technological advances are changing business and operating models, which is challenging to an industry that’s accustomed to slow evolution rather than rapid transformation.

Getting up to speed demands a clear strategy and roadmap for decommissioning legacy systems, accelerating automation, and laying the platform for the next wave of transformation

Still a need for longer-term transformational change

There is the other side of the coin when it comes to the described optimism and opportunities. 66% of insurance CEOs still report increasing pressure on their organisation to deliver business results under shorter timelines and more insurance CEOs see changes in consumer behaviour as a threat to growth [78%] than almost any other sector.

So while perhaps having overestimated the impact of outside threats and short-term disruption, insurers shouldn’t be underestimating the need for longer-term transformational change into digitally-enabled, customer-focused organisations with flexible business and operating models.

Driving innovation requires a dialogue between human and machines in a ‘bionic’ organisation. This isn’t about one dictating terms to the other, but humans communicating with AI and robotics to mutually improve outputs. Key to this transformation will be the success to attract digital talent, but at this point only 19% of insurance CEOs say it’s easy to do so.

More than 80% are concerned about shortages of digital skills within the industry [81%] and within their workforce [86%]. While this is a challenge for all sectors – around three-quarters of participants in the CEO Survey are concerned – insurance CEOs are most concerned.

And it isn’t just digital skills that are in demand, but also the creativity and emotional intelligence needed to innovate and reconnect with customers. 86% of insurance CEOs believe they need to strengthen soft skills in their organisation alongside digital skills.